07 Mar 2022

Retire on your own terms, not just at 65

In the knowledge economy, and particularly in domains like financial advisory, the quality of service is often tied to the longevity of the service provider. Professionals with decades of experience under their belt often merit more credibility than their younger counterparts. So, why retire specifically at, say, 65, and give it up when you’re top of the game?

This is the question eliciting considerable opinions and discussions in recent years. Encouraged by increasing life expectancies, medical breakthroughs, and non-conventional approaches, many are questioning conventional notions surrounding “retirement age”. Such notions do not hold water anymore, with industry veterans showing no signs of stopping anytime soon.

"If you retire, you stop contributing to the economy. After that, you’re merely a consumer"

“In 1977, the manufacturer “retired” a Premier Padmini car model, putting it out of use. Can we use the same “retirement” analogy to talk about a 65-year-old professional in the knowledge economy? We absolutely cannot. If you retire, you stop contributing to the economy. After that, you’re merely a consumer,” said Ashok Sardana, Founder and Managing Director of the Continental Group, a leading insurance intermediary and financial services solutions provider in the GCC region.

“But regardless of whether or not you want to retire, and when you want to retire, it is important that you base your decisions on your own terms. And to do so, you must undertake financial planning,” added Sardana, who is a lifetime member of the Million Dollar Round Table (MDRT) and a top-of-the-table qualifier for over 20 years.

Financial planning: The sooner the better

The link between retirement and financial planning formed the basis for the latest webinar(1) by the Continental Group. Titled ‘Retire on your own terms, not just at 65’, the webinar touched upon the evolution of “retirement” as a term, its financial implications, and key considerations in the planning process. A notable takeaway from the webinar was the consensus on the need for early financial planning. In the audience poll on the advisable age to start retirement planning, 69% of respondents stated age 35-40, 26% of respondents state age 40-45, and around 3% stated age 45 and above.

As opposed to a conventional process, where you determine how much wealth you need for retirement, secure it, and burn it backward; an early financial planning involves an accumulation phase, a consolidation phase, and the final phase of succession. Early financial planning isn’t about fixing a certain number for retirement. It’s about incrementally increasing your savings and simultaneously hedging them against risks. Proponents of this approach often diversify their portfolios, invest in key considerations such as health and life insurance, and ensure their family’s financial security.

Balancing risks and rewards through diversification

When you’re in your 40s and envision your financial future, there are multiple considerations: Will my spouse have enough wealth if I fall ill? Do I want to live closer to my children when I’m old? Should I make a living will and edit it as per change in circumstances? Such questions are commonplace, and rightly so because, despite the general increase in life expectancy, we can never know what tomorrow has in store. So, even if it means putting away minuscule savings at a young age, it will be worth it — and more so if you diversify your holdings.

Thematic equities with long-term growth prospects, bonds, and fixed income deposits are all good options, even if they mean longer lock-in periods and low-interest rates. “The essence of diversification is to hedge against investment risks. You can set short and long term targets, factor in inflation, and evaluate the risk you’re willing to take at every stage,” said Rickson D’Souza, a leading financial consultant and a top-of-the-table MDRT qualifier who holds a seat reserved for top 1% financial advisors in the world.

“Investments in stocks, bonds, and oil futures are attractive options, which can fetch high returns. But the pendulum swings both ways — higher reward also accompanies higher risk. So, as you age, it is advisable to reduce your exposure to volatile investment avenues, and shift instead to low-risk alternatives like fixed deposits,” D’Souza added.

The essentiality of health, life, and disability income insurances

As often as not, insurance is viewed as discretionary spending. But they are an investment in a secure financial future. Most professionals continue to be under group coverage, which can be altered by employers. If the professional is diagnosed with a serious illness or meets with an accident, and is unable to continue with employment, the group insurance will not suffice. To make matters worse, the chances of getting new insurance thereafter is hampered due to pre-existing condition. In such circumstances, an existing personal health or disability income insurance can change the course of your financial future.

Insurance will help sustain financial obligations, like children's education fees, rents, bills, etc. while allowing full focus on recovery. Even life insurances make a compelling case as far as retirement financial planning is concerned. They are part of the financial legacy that one can leave behind in the event of an untimely demise, ensuring the financial security of the family. As you grow older, you can reallocate the life insurance investments into other avenues and new purposes, including activities like traveling, etc.

"Worry less about retirement and concentrate more on retirement financial planning"

The pursuit of new purposes, as part of the retirement plan, was substantiated in another Continental Group audience poll. Around 78% of the respondents said they want to enjoy life and experience things they put on hold because of their careers. “If you choose to retire from your profession, it is important to secure a new purpose. I learned this early on, based on the life of my father. He retired at 65 in spite of my suggestion not to. And he soon found himself without a new purpose. So, I advise clients to worry less about retirement and concentrate more on retirement financial planning,” said Ashok Sardana, in closing.

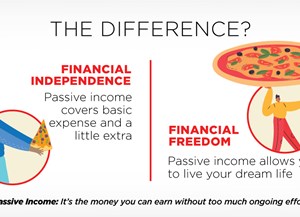

Read more on The difference between Financial Independence and Financial Freedom and how planning your finances can help you retire early.

For experts advice on retirement financial planning connect with us on Clientservice@cfsgroup.com.