Electric Vehicles cost more to insure than petrol cars in UAE

Electric vehicles (EVs) are more expensive to insure in the UAE than their traditional fuel-powered alternatives.

This is due to the higher number of claims, cost of repairs and parts, and the fact that some drivers are not used to them, industry experts told AGBI.

“It’s true that some insurers price electric and hybrid car premiums higher than ICE [internal combustion engine] cars due to the cost of repairs,” said Faisal Abbas, head of general and medical insurance at Dubai-based insurance broker The Continental Group.

Saudi Arabia likely to see two more electric vehicle plants

One of the factors pushing up the cost of EV insurance is how expensive their parts are in the Middle East, said Mina Sahib, insurance business director at XA Group, a Dubai-headquartered company which offers automotive aftersales and repair services.

“There are many factors that impact the pricing of motor insurance premiums but certainly the more expensive the risk, the more expensive the premium will be,” Sahib said.

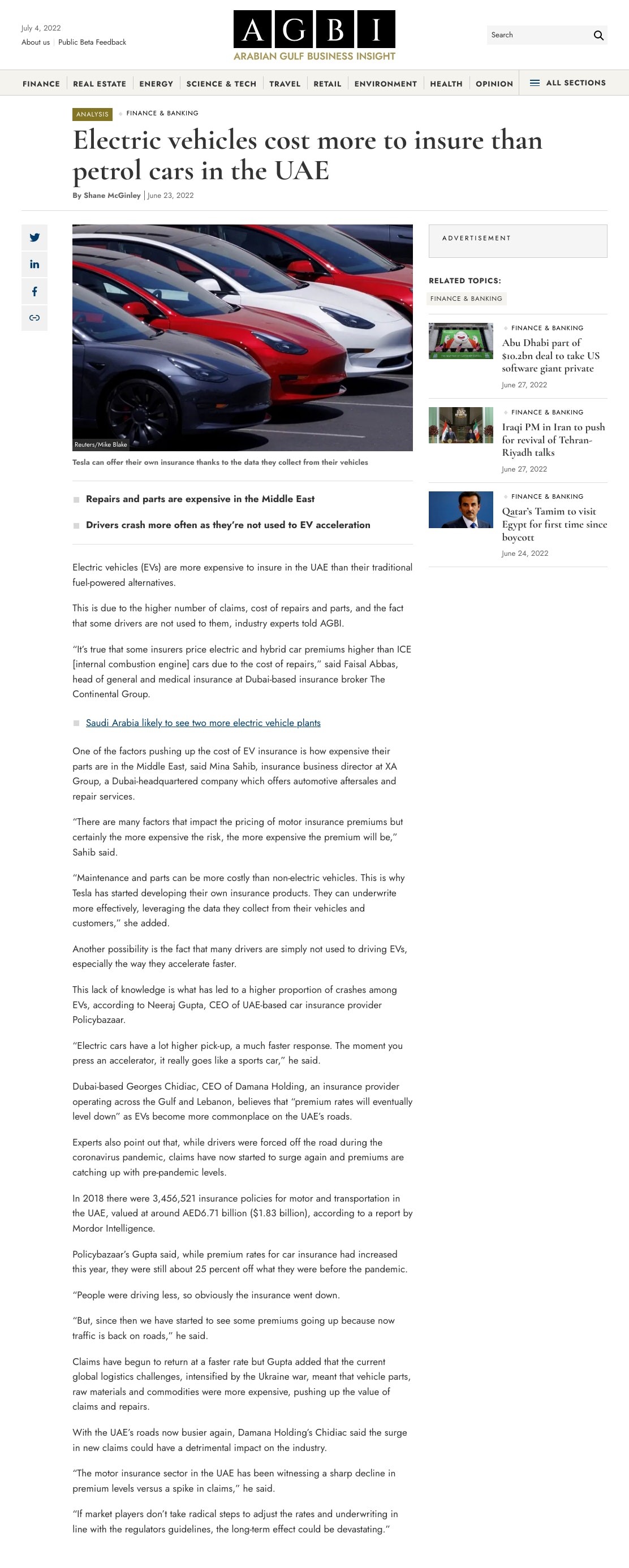

“Maintenance and parts can be more costly than non-electric vehicles. This is why Tesla has started developing their own insurance products. They can underwrite more effectively, leveraging the data they collect from their vehicles and customers,” she added.

Another possibility is the fact that many drivers are simply not used to driving EVs, especially the way they accelerate faster.

This lack of knowledge is what has led to a higher proportion of crashes among EVs, according to Neeraj Gupta, CEO of UAE-based car insurance provider Policybazaar.

“Electric cars have a lot higher pick-up, a much faster response. The moment you press an accelerator, it really goes like a sports car,” he said.

Dubai-based Georges Chidiac, CEO of Damana Holding, an insurance provider operating across the Gulf and Lebanon, believes that “premium rates will eventually level down” as EVs become more commonplace on the UAE’s roads.

Experts also point out that, while drivers were forced off the road during the coronavirus pandemic, claims have now started to surge again and premiums are catching up with pre-pandemic levels.

In 2018 there were 3,456,521 insurance policies for motor and transportation in the UAE, valued at around AED6.71 billion ($1.83 billion), according to a report by Mordor Intelligence.

Policybazaar’s Gupta said, while premium rates for car insurance had increased this year, they were still about 25 percent off what they were before the pandemic.

“People were driving less, so obviously the insurance went down.

“But, since then we have started to see some premiums going up because now traffic is back on roads,” he said.

Claims have begun to return at a faster rate but Gupta added that the current global logistics challenges, intensified by the Ukraine war, meant that vehicle parts, raw materials and commodities were more expensive, pushing up the value of claims and repairs.

With the UAE’s roads now busier again, Damana Holding’s Chidiac said the surge in new claims could have a detrimental impact on the industry.

“The motor insurance sector in the UAE has been witnessing a sharp decline in premium levels versus a spike in claims,” he said.

“If market players don’t take radical steps to adjust the rates and underwriting in line with the regulators guidelines, the long-term effect could be devastating.”